Everything You Need To Know About Applying For Financial Aid

Updated January 13, 2023

CollegeChoice.net is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Turn Your Dreams Into Reality

Take our quiz and we'll do the homework for you! Compare your school matches and apply to your top choice today.

The Complete Guide to Getting Your Money

The words "Financial Aid" are enough to send chills down the spine of any potential college student or parent because people think that the process for applying for aid is time-consuming and bureaucratic. They aren't wrong.

Here at College Choice, we've made this efficient, streamlined tutorial for navigating your FAFSA app. With our guide, you'll cut your application time in half and complete it stress-free because you'll know what's coming and exactly what to do on the app—no learning as you go!

On this page you will find:

- Checklists for what you'll need to have at the ready and step-by-step pics of the process

- Tricks for protecting your own savings accounts and other financial assets

- A list of common mistakes that people make which often cost more funding

- Simple ways to determine your qualification and dependency status

So, let's have a go at it and you all the information you need to assess your eligibility for federal aid, traverse the app, and get your funding.

Pour that coffee, take a seat, and let's get this F-A-F-S-A done N-O-W!

What is FAFSA?

The FAFSA, or the Free Application for Federal Student Aid, is a form filled out by students (and - more often than not - parents) to apply for federal loans, work study funds, and grants. The Department of Education, which is responsible for administering FAFSA, provides more than $150 billion in financial student aid every year.

Generally speaking, there are two kinds of funding for students: Merit-based aid and need-based aid:

- Merit-based scholarships are applied for independently of the FAFSA and are awarded through schools and private institutions and given out for achievements and academic performance.

- Need-based scholarships take your financial status solely into account to establish a loan. Factors include your mean income, your assets, and the cost of tuition.

If you're thinking that taking out loans for your education is too tough or too complicated, think again. FAFSA has made it easier than ever to fill out and application and get started. As well, getting a college degree is still the closest thing to a guarantee for gaining meaningful employment in the United States. Take a look at this unemployment data related to completing a college degree and the increase in the likelihood of landing a job:

As well, grants and scholarships account for a massive percentage of how people pay for school, so you aren't in it alone. Spending on college is very much tethered to borrowing money and paying it back later:

With all those considerations in mind, let's take a look at how to get the FAFSA process started.

How Can I Predict the Aid I Will Get?

Your eligibility for federal loans (which are paid back to the government after you leave school) and federal grants (which do not have to be paid back) is determined by information you provide on your application.

Even if the forecaster designates your family's assets and income out of the range of grants, you should still complete the FAFSA since many colleges, foundations, and state scholarship organizations use the FAFSA to distribute money and determine scholarship funding. Plus, filling out the FAFSA qualifies you for low-cost federal student loans of at least $5,500 per year, so you have nothing to lose but a couple hours by filling it out. And after our preview, you can cut that time in half.

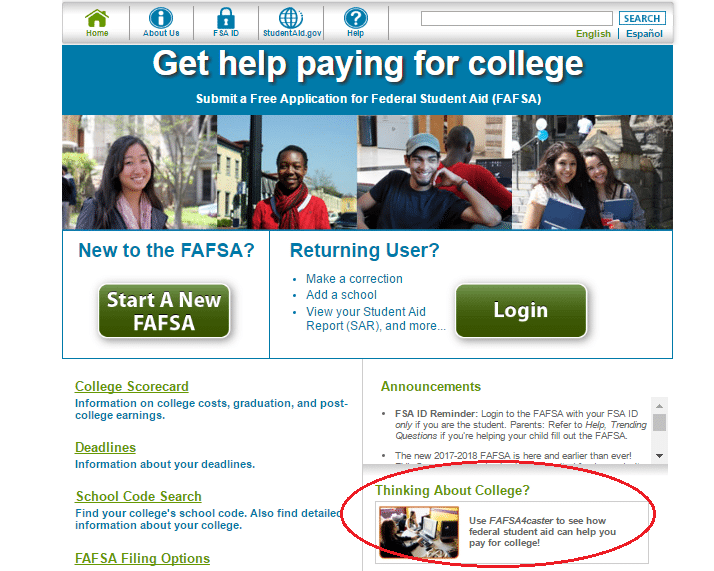

You might be wondering if you're eligible to receive FAFSA money, which is a common question among prospective students. To determine whether or not you're eligible for student financial aid, it is recommended that prospective students and parents visit the FAFSA4caster site.

Through this site, you will enter information about your income, home, tax status, savings, and other factors related to paying for school. The more information you can enter, the more accurate the estimate will be, so be sure to have last year's tax docs, a pay stub, and your banking information at the ready!

To get started with the FAFSA4Caster, click here and then click the box "Thinking About College."

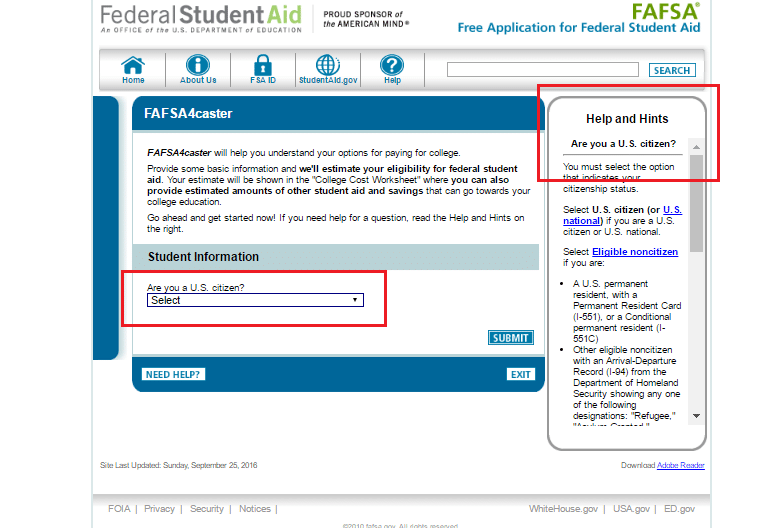

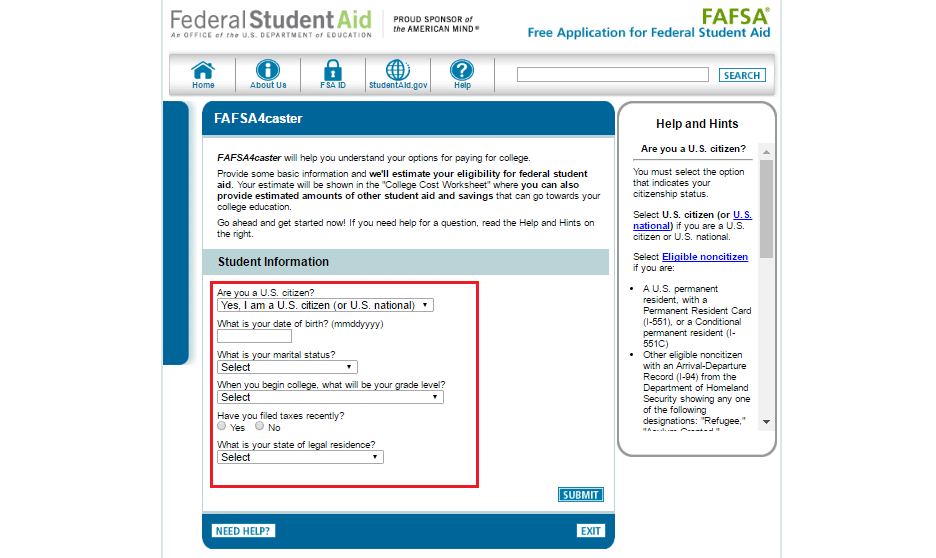

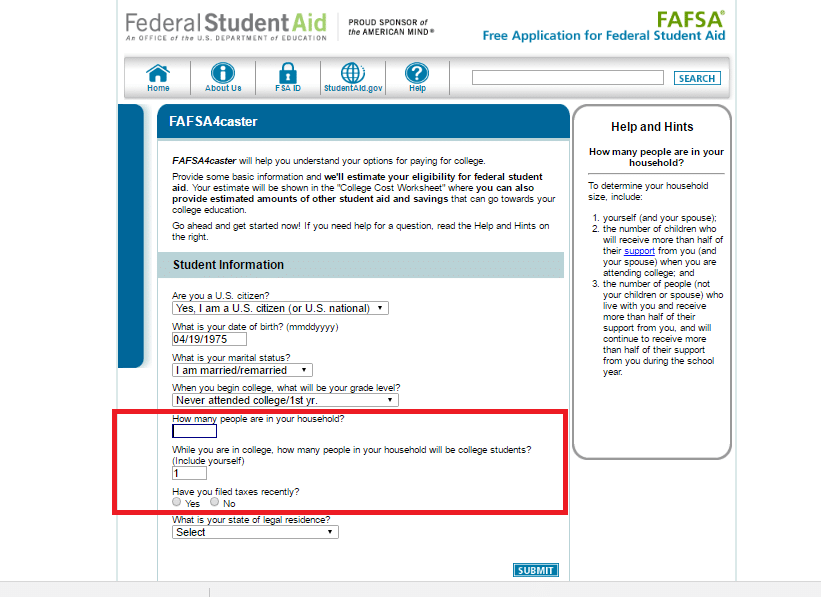

Once there, click the pull down menu indicating your citizenship status, which will initiate another series of necessary information including you DOB, marital status, grade level, tax update, and state of legal residence. Also, take note of the helpful box that follows you and answers your questions!

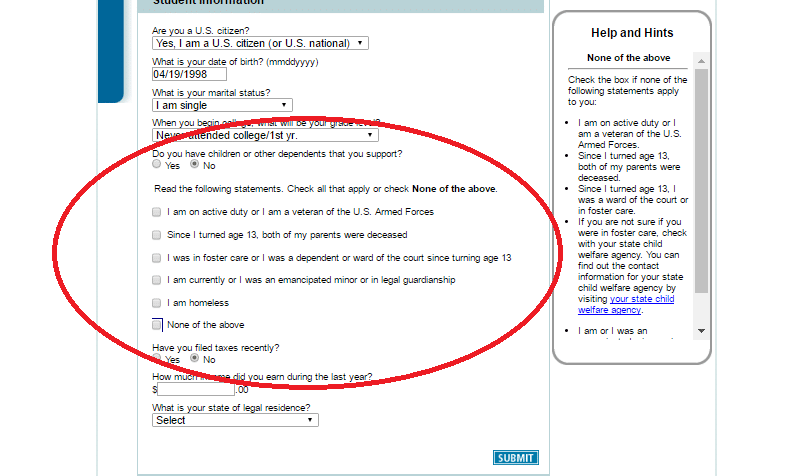

If you have no children or dependents, you will be prompted with a series of boxes that will help you determine your dependency status.

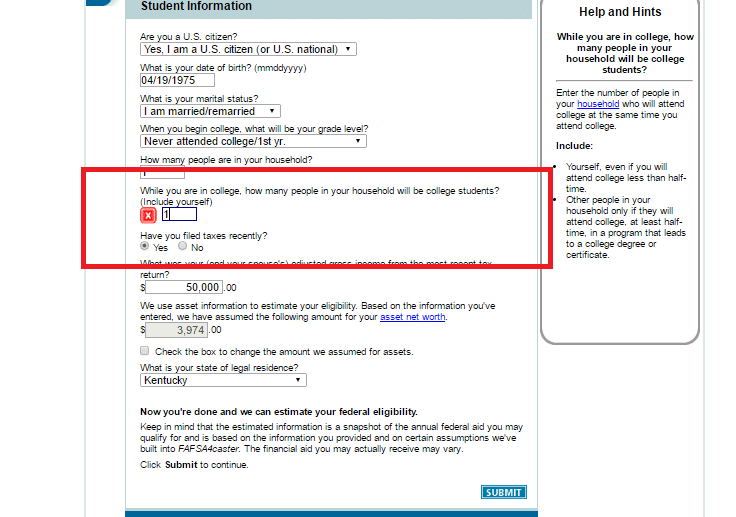

You will then answer questions about your household and the number of people in your household who will also be going to college. Be sure to put at least a one in there!

If you forget to fill in a box, or the system catches your misinformation, you will be prompted to go back and fix the issues - not the red X and the solution to the problem. Fix it and move on!

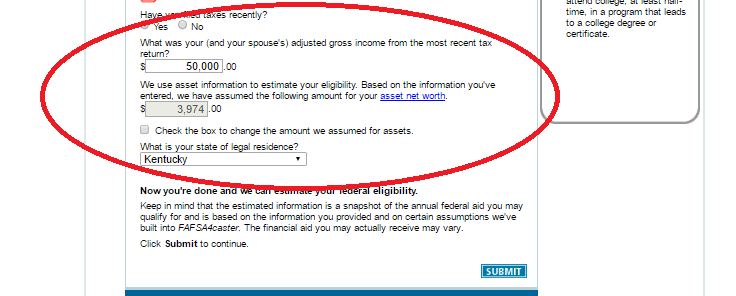

Enter your income based upon your dependency status. If you're married, factor in your spouse's income, too.

Now that you've completed that, you're one step closer to knowing how much aid you'll receive, but you will now need to enter exact or estimated costs related to money that you will receive, or think you will receive.

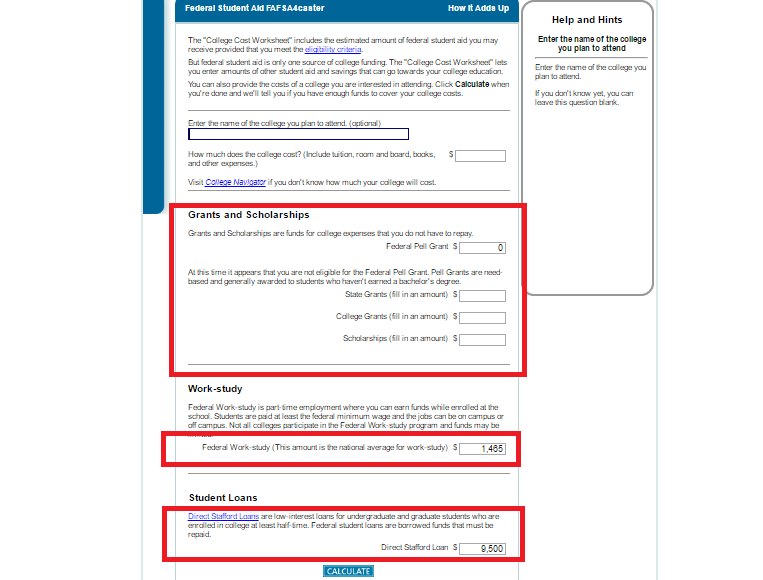

There are four basic categories for financial aid. In a moment, we'll see how the the calculator on the FAFSA forecaster site will organize your funding information into these categories, but here's a brief look at what kinds of funding you can receive:

> Grants and Scholarships

These are funds for college expenses that you do not have to repay, such as:

- Federal Pell Grant (which you access by filling out a FAFSA)

- State Grants (which you apply for through your state government or gain access to in a variety of other ways, like money earned though course credit in high school)

- College Grants (monies given to you by the institution you'll be attending)

- Scholarships (like money from organizations or businesses not related to the aforementioned sources)

> Work-study

These funds are derived from part-time employment where you can earn money while enrolled at the school. Students are paid at least the federal minimum wage and the jobs can be on or off campus, depending on the needs of the university. To be clear, not all colleges participate in the Federal Work-study program and funds for these programs are limited. As well, it might be advantageous to forgo trying to get a work-study position in favor for more lucrative part-time work as you move through college.

> Student Loans

These funds are the monies you will borrow from the government that will have to be paid back. These loans are low-interest and are given to undergraduate and graduate students who are enrolled in college at least half-time.

Payments on your loan will begin once you:

- Graduate (You have a 6-month grace period to find a job!)

- Drop out (Don't do it! You can finish this!)

- Drop below half-time status. (Just do a little bit at a time!)

Should you not return to school after borrowing money from the government, you will still have to pay the money you borrowed back. If you graduate, you are given a six-month grace period before having to make monthly payments on your school loans.

> Additional Resources

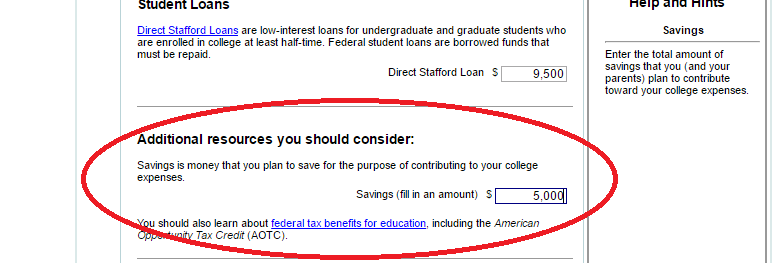

Lastly, the FAFSA estimation calculator takes into account any other potential funding sources. Savings, gifts, and other monies which you've set aside for the purposes of furthering your education will be considered in this category.

Now that you understand the different kinds of funding, you can move to selecting your schools and entering specific information about funding.

Here's a look at what the page looks like on the whole. Note all four categories are represented and that the calculator is already accounting for Direct Stafford Loans (low interest loans you receive as long as you're enrolled in school half time) and Work-study funds:

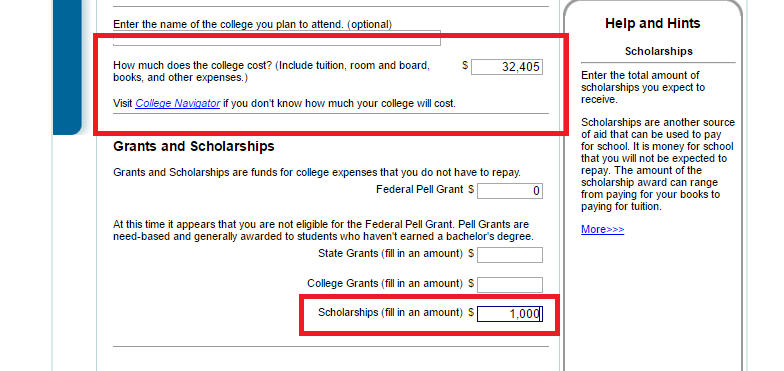

Let's say you know you want to attend a private school, but you don’t know which one. Go ahead and enter one of the following averages that corresponds to the kind of school you’d like to go to - private, public in-state, or public-out-of-state:

- $32,405 for a private college education

- $9,410 for a state resident attending a public college

- $23,893 for an out-of-state resident attending a public college

Or maybe you know exactly where you're going and can even enter some scholarship info. Go ahead and do it:

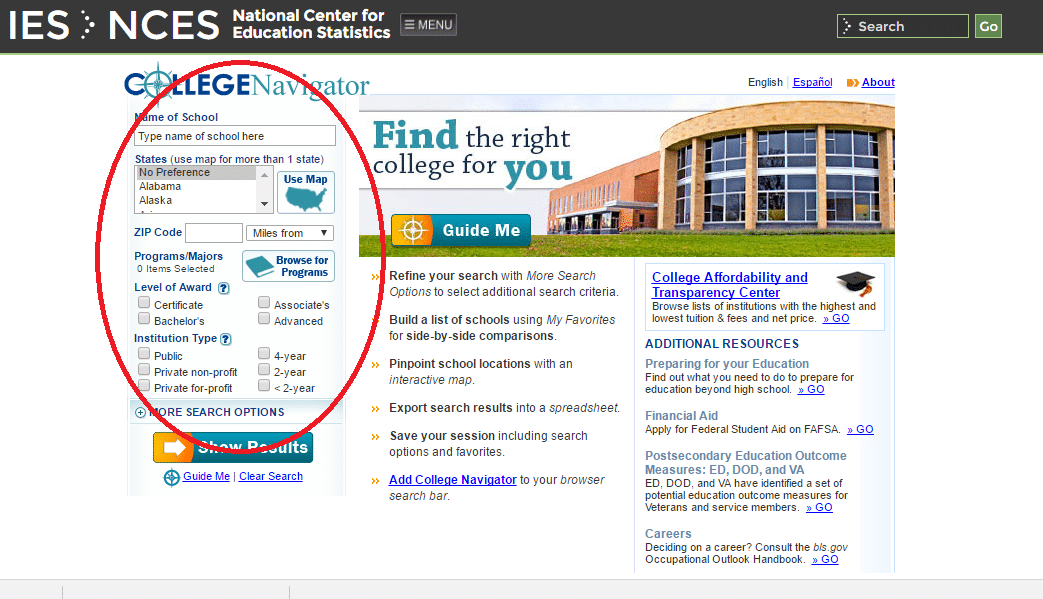

But, if you want to broaden your search or estimate for more than one school, the College Navigator tool, which will take you to another site where you can answer specific information about the colleges of your choice and get an exact number to enter into the calculator, will be really helpful!

Once you've entered the desired information, go ahead and enter any additional resources you can estimate contributing:

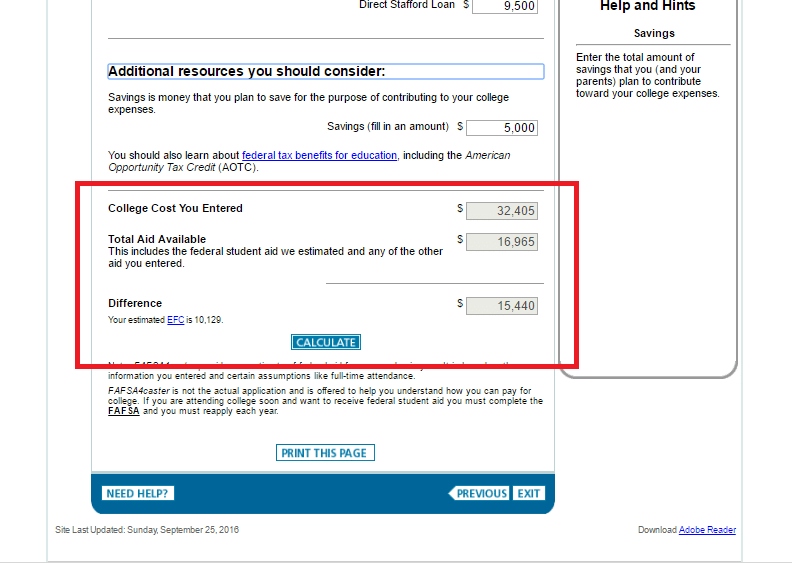

Almost done! Just hit calculate and you'll get an estimated cost for what you will have to pay out of pocket. This is the estimated amount of money you will take out in FAFSA money, which will be paid back after you graduate, drop out, or drop below half-time status.

That's it! Now you have a good estimation of what it will cost you to complete school!

How Do I Apply for FAFSA?

Once you've determined your estimated yield for student aid, you can apply to FAFSA online at fafsa.ed.gov, on the telephone at 1-800-433-3243, or by paper application (available on the FAFSA website). The FAFSA application becomes available October 1st and closes June 30th the following year.

If you're filling out your information for the first time, be sure to block out an hour to complete the task. Each year, you will have to reapply for aid by filling out a renewal FAFSA. A renewal takes far less time because you simply need to update your information before submitting. It is advised that you submit your FAFSA application as early as possible.

When you apply, you should have the following materials within reach:

Your FSA ID

If you're filling out your app, you will need a FSA ID. This ID will get you into the system and will be used for later access as well. The ID is free.

Your Social Security Number

You can locate your SSN on your Social Security Card. If you don't have your SSN card, the number may be on your birth certificate or permanent resident card. If you are not a U.S. citizen, you'll also need your Alien Registration Number.

Your Driver's License Number

This number, located on your driver's license, could be used in the verification process. If you’d don't have a driver’s license, they you will not have to concern yourself with this step.

Your Tax Records

You will need your taxes from either one of the two previous tax cycles. You can also import your tax data by using the IRS Data Retrieval Tool, which will save you a lot of time.

Untaxed Income Reports

This will include a variety of monies including things like received child support, interest income, and veteran’s non-education benefits.

Asset Records

Savings and checking account balances, information about investments like stocks, bonds, and real estate are all pieces of information that you will have to report.

List of Schools

Be sure to have a list of schools that should review your FAFSA. Your FAFSA information will go directly to schools for consideration. You will be prompted to add 10 schools, with the ability to add more at a later time. Add schools you're considering, even if you're not sure if you want to go to them.

And don't be afraid to get help from those nice folks at the FAFSA office!

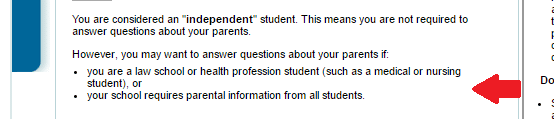

Am I Dependent or Independent?

If you're an independent student, you will report your own personal information, and - if you’re married - your partner's information. If you're a dependent student, you will report your and your parent's information. You can determine your dependency status on the FAFSA website. You can also use this handy infographic from the FAFSA site.

As well, the FAFSA site offers directives for individuals in foster care, emancipated minors, legal guardians, and homeless. Here is information directly from the FAFSA site to help you determine your aid needs:

- Will you be 24 or older by Dec. 31 of the school year for which you are applying for financial aid?

- Will you be working toward a master's or doctorate degree (such as M.A., M.B.A., M.D., J.D., Ph.D., Ed.D., etc.)?

- Are you married or separated but not divorced?

- Do you have children who receive more than half of their support from you?

- Do you have dependents (other than children or a spouse) who live with you and receive more than half of their support from you?

- At any time since you turned age 13, were both of your parents deceased, were you in foster care, or were you a ward or dependent of the court?

- Are you an emancipated minor or are you in a legal guardianship as determined by a court?

- Are you an unaccompanied youth who is homeless or self-supporting and at risk of being homeless?

- Are you currently serving on active duty in the U.S. armed forces for purposes other than training?

- Are you a veteran of the U.S. armed forces?

If you answered no to the above material, you may be considered a dependent student and will most likely need your parent’s financial information when you work on your FAFSA application.

If you answered yes to the above material, you may be considered an independent student and may not be required to enter your parent’s information.

Do I Qualify for FAFSA?

Almost every student is eligible for some kind of financial aid. And, even if a student doesn't qualify for need-based aid, they may qualify for an unsubsidized Stafford Loan (a loan where the federal government doesn't pay the interest on the loan) regardless of income or circumstance.

To be eligible for federal financial aid, an applicant must:

- be registered with the Selective Service System.

- maintain a C average minimum GPA (or a higher minimum set by the student’s institution of choice).

- is a U.S. citizen, a U.S. national, or an eligible non-citizen.

- has a valid Social Security number.

- has a high school diploma or GED.

- sign a certification statement stating that the applicant is not in default on any current loans or owes money on a federal student grant and that federal aid will only be used for educational purposes.

- has not been found guilty of possession of illegal drugs while federal aid was being received.

If you're thinking you might go to college and do a little partying on the government's dime, you may want to think again. In 2010, the Student Aid and Fiscal Responsibility Act (SAFRA) changed its conditions for suspension of eligibility for drug-related offenses.

Before, students could lose eligibility for either the possession or sale of controlled substances during their enrollment period. SARFA increases the suspension to two years for the first offense and an indefinite period for the second offense.

It's clear: drug use and student loans don’t mix. If you take out a loan for school, the only thing you should be getting high on is knowledge.

In addition to these rules, there are some recent developments for military veterans and active duty service people. With this, education and housing related benefits for these personnel through the Post 9/11 G.I. Bill and the Yellow Ribbon program, the amount of military aid a student receives for post-secondary education does not defer eligibility or reduce the amount of student aid that a student can receive from Pell, SMART, FSEOG, or TEACH grants.

The FAFSA Step-By-Step

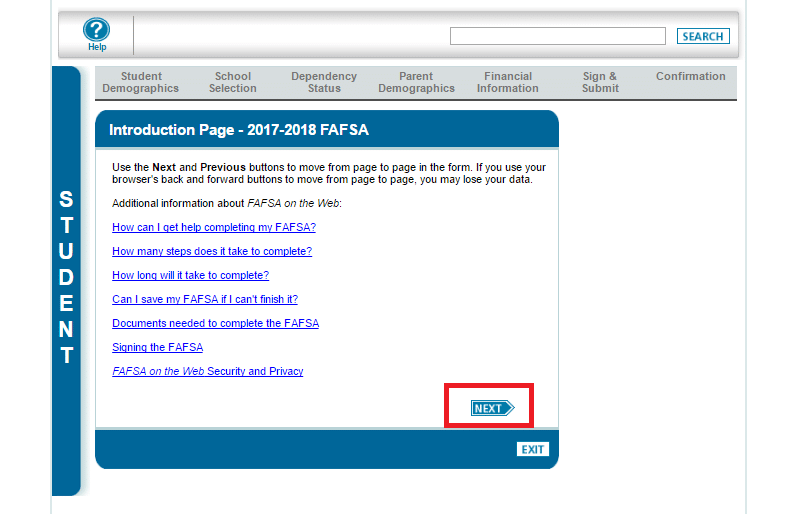

Well, here we are - you've learned everything you need to know about what you need and what you need to know about the FAFSA submission process, so let do this! Go to fafsa.ed.gov!

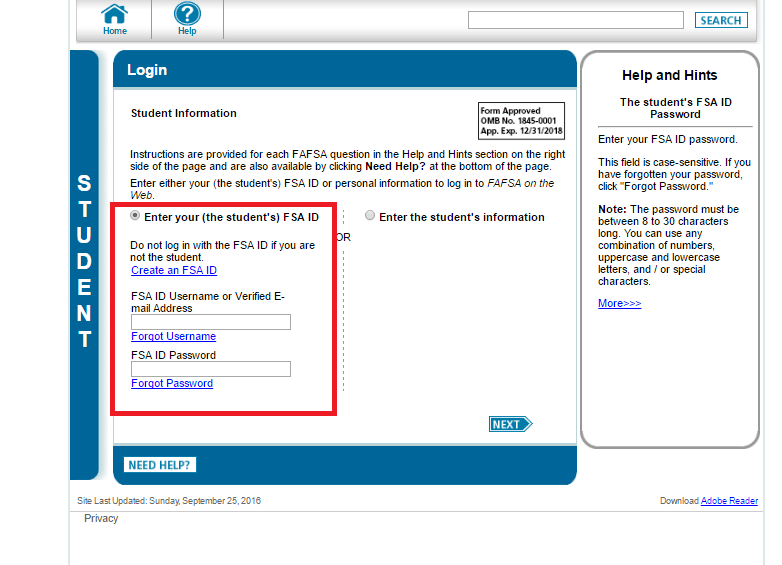

First, You'll need a FAFSA ID. If you have one, you'll be prompted to enter your info like this:

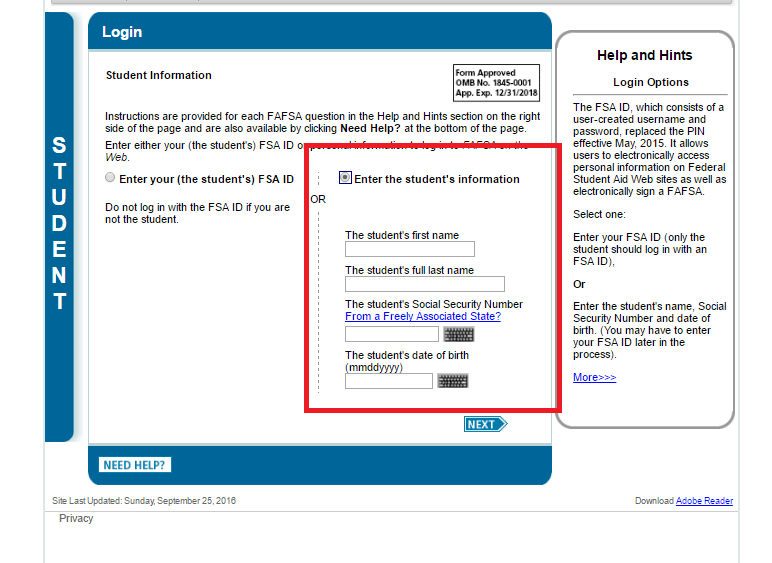

If not - no problem! Just enter the information requested:

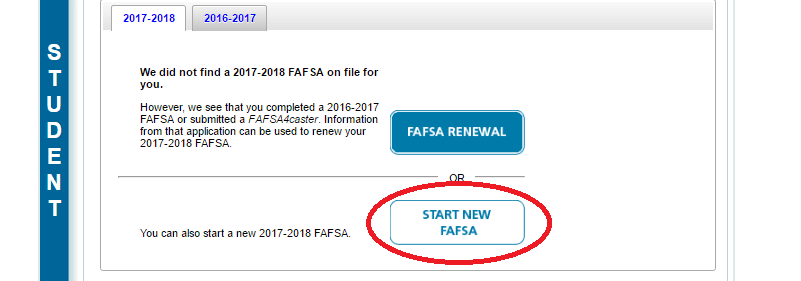

You'll then be prompted with whether or not you want to renew your old information (very, very simple - if you’re choosing that option, you don't need any help!) or if you want to start a new FAFSA. Pick start a new FAFSA.

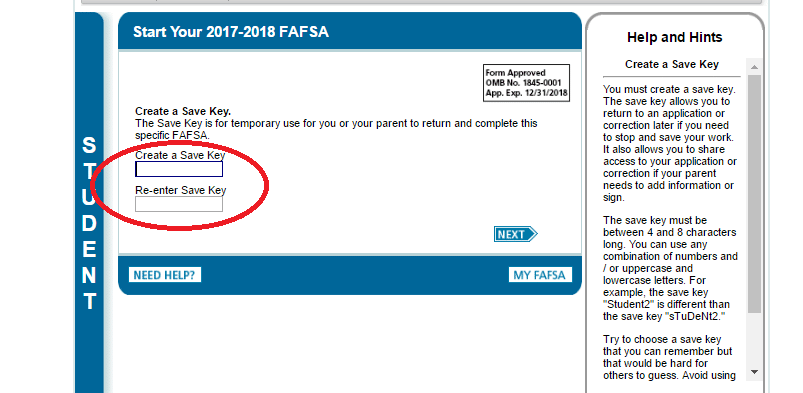

Then create your "Save Key" which you will need to complete the specific FAFSA you're working on. If your computer fails or you can't finish it in one sitting, you'll come back and enter this code. Be sure to write it down!

Next, a screen will appear with hypertext and FAQs, which you won't need because you've already scanned this excellent web page for all the info you could possible want 😉

Click "Next" to move on!

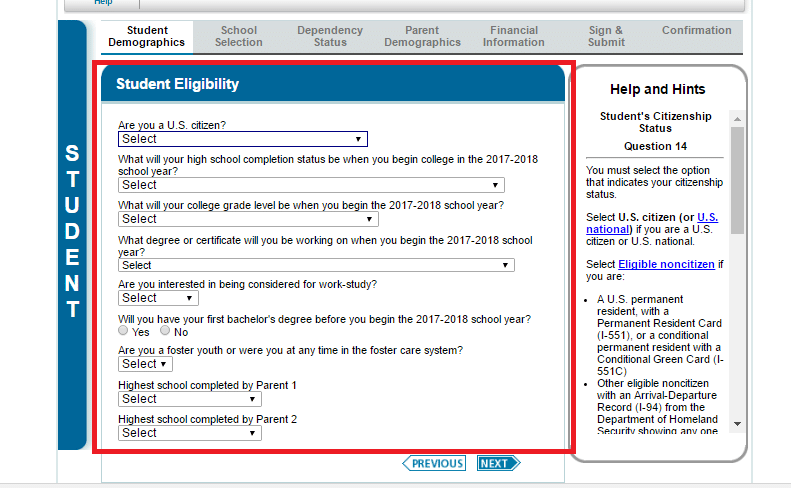

Now, slog through entering all that info about yourself and hit "Next."

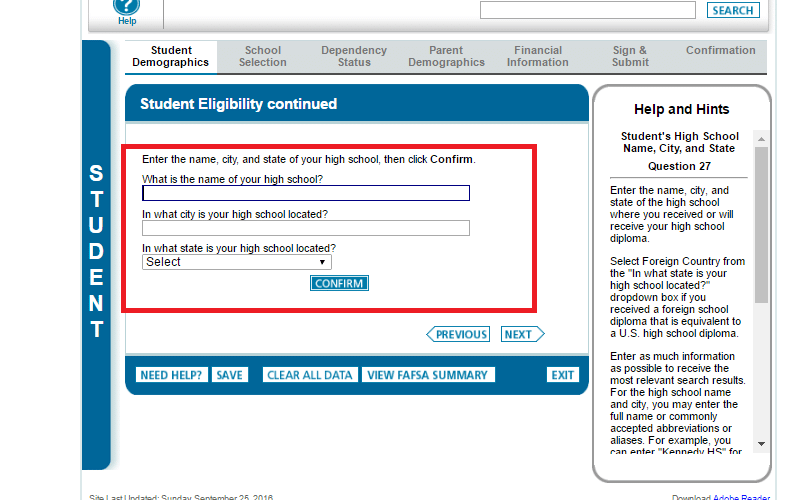

Then some demographics info (Ugh, but required) and information about your high school education. Click "Confirm."

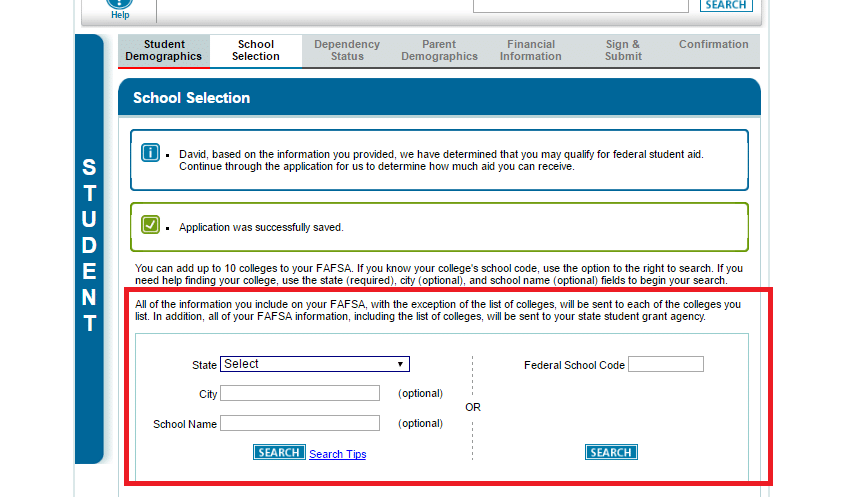

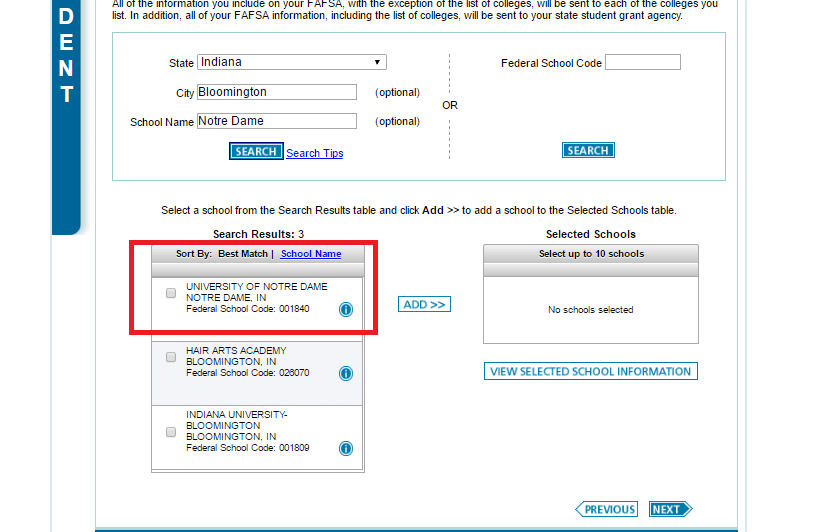

Look for that green check, which means you can move forward! Now, a fun part! Where are you thinking of going? Enter the information using the pull-downs; that is, unless you know the Federal ID code:

Looks like someone might need to watch "Rudy" again if they think Notre Dame is in Bloomington... That’s "Hoosiers!" - jeez!

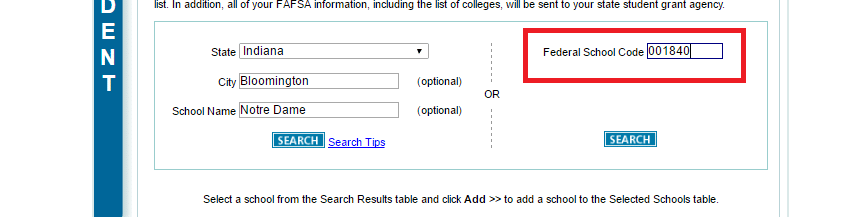

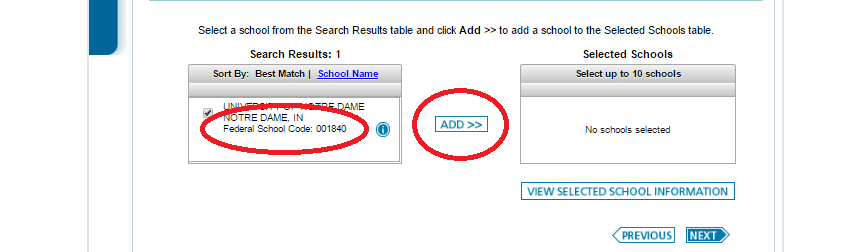

Get the school code from the search and enter it in the adjacent column:

Then "Add" the school to the next column. You can repeat this process with up to 10 schools that you would like to receive your FAFSA information.

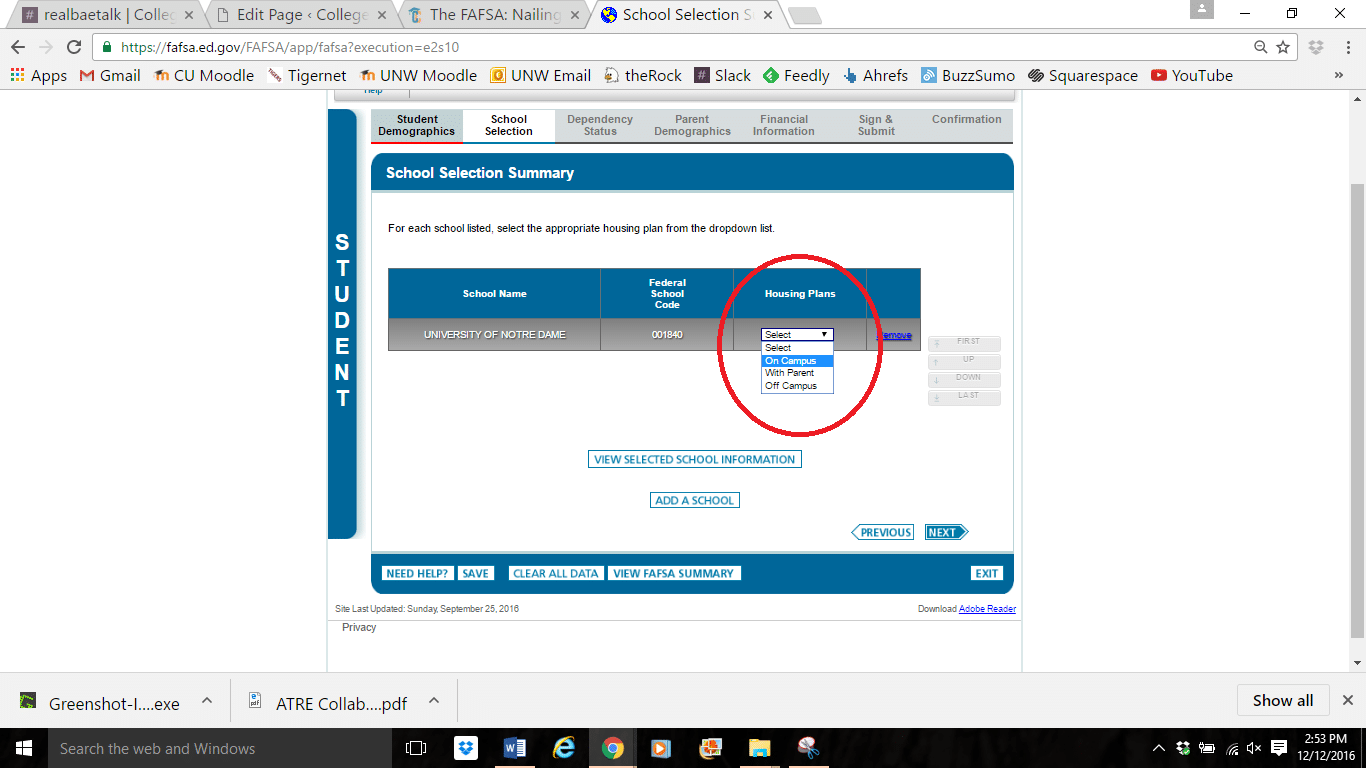

Now you can tell the folks over at the FAFSA office (and the schools of your choice) what your living situation will be. Use the drop down menu to select it.

Look for that green check again!

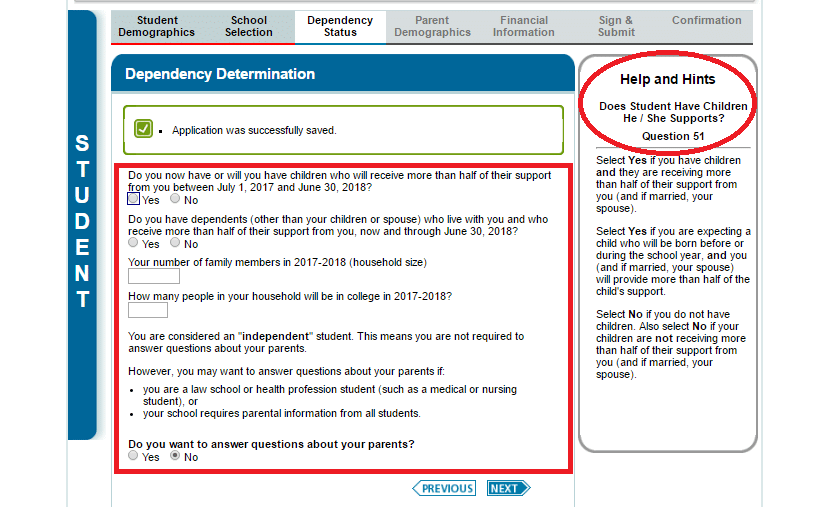

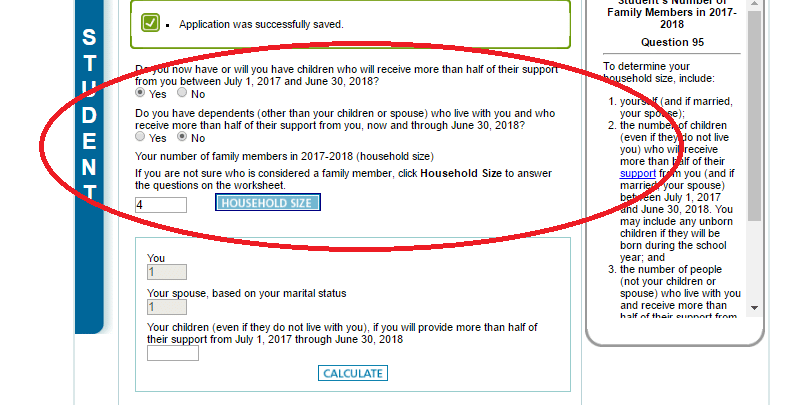

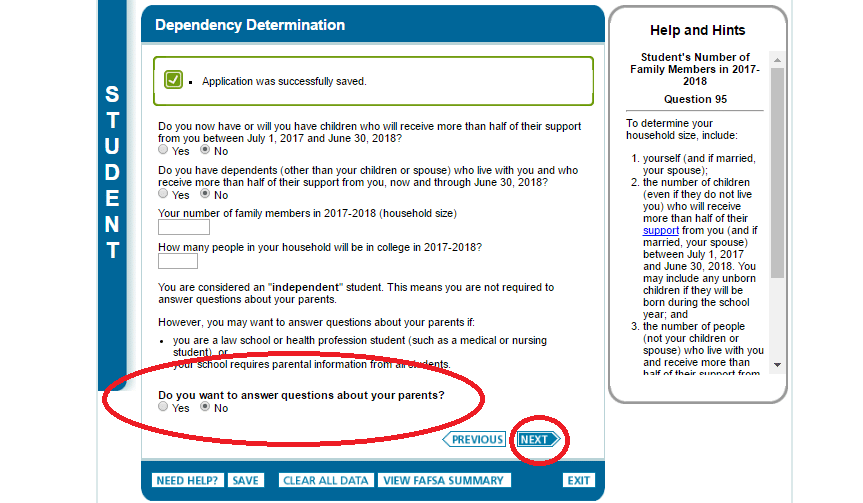

Now you can move on to your next category, "Dependency Determination." Go ahead and enter the correct information concerning your dependency. If you get stuck, scroll up and take a look at our dependency checklist, or use the "FAFSA Help" window.

If you have dependents, enter the correct information:

If not, go ahead and let your parents take care of the hard stuff! Click "Next."

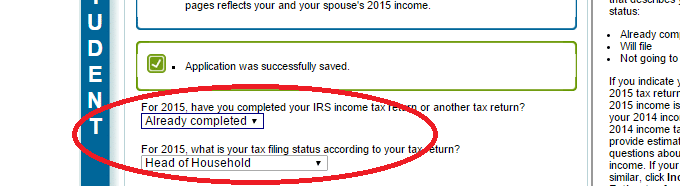

If you're independent, FAFSA will give you this little reminder, and then the option to access a previous tax return:

Answer the questions about how you filed in the previous year of your tax filings:

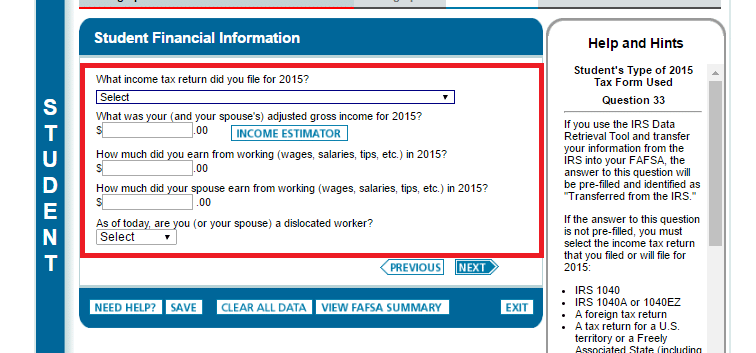

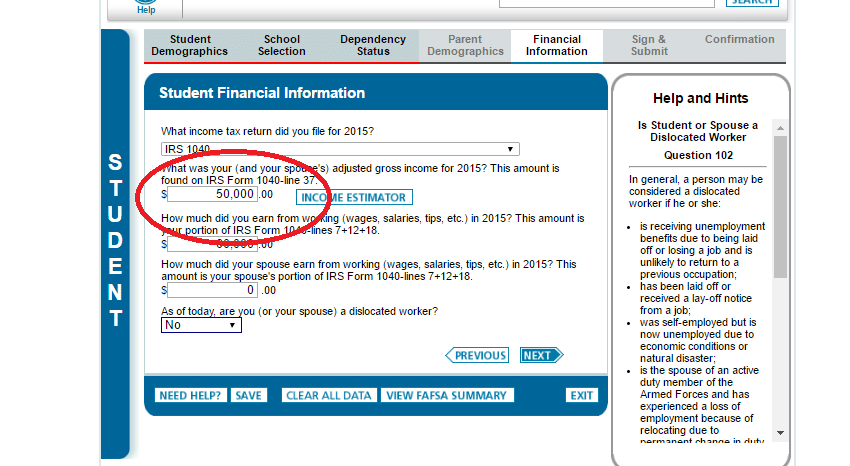

Now you will answer questions about your income and wages - all simple stuff if you have you have those resources we suggested above at your fingertips!

Go ahead and fill out all the information, like so:

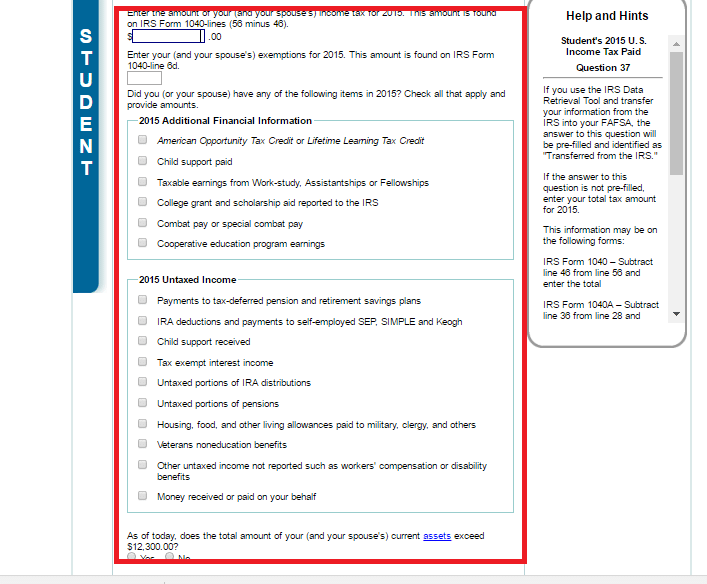

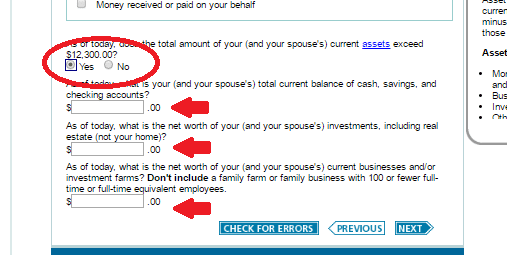

Then the big daddy - check all that apply:

And don't forget to disclose your assets!

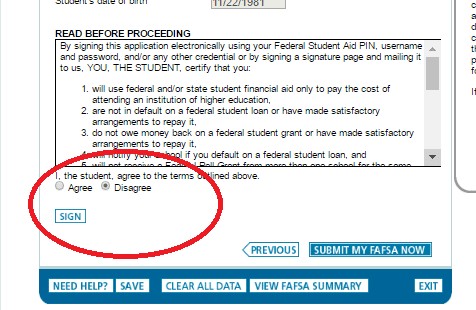

Once you do that, agree to the terms and sign that sucker to apply!

You're done! Pour yourself a glass of wine and take the rest of the day off!

What Are the New Changes to FAFSA This Year?

The FAFSA is the form each student must fill out to receive financial aid in the form of grants, loans, and work study exchanges. Also included are scholarships from the state and the educational institution. To receive any of these monies, students should fill out this form as soon as possible.

There’s good news, too, for students filling out the FAFSA this year, as substantial changes have recently been made:

Change #1: Early Extension

Previously, the FAFSA became available for completion on January 1st. With the new changes, the opening of the application has been moved back a full two months!

Students can now begin filing for financial aid as early as October 1st. This is good news, as student financial aid is given out on a first-come, first-serve basis.

Change #2: Two-Year Tax Return

With the new changes, active tax returns from two years prior to the date of submission are usable for the application process. Called the "prior-prior" rule, this makes the submission process simpler by giving the applicant more time.

FAFSA and Asset Management

Here's the real deal when it comes to the particularities of investments when it comes to filling out the FAFSA. Remember, capital gains are treated as income - that's the reality. While your kid is still in high school, you need to cash in those securities and begin managing your money differently.

Here's what does have to be reported: CDs, stocks, bank and brokerage accounts, bonds, mutual funds, college savings plans, trust funds, real estate, and money market accounts.

Here’s what doesn’t have to be reported: home equity, qualified retirement plans (pensions, annuities, IRAs, 401(k)s, and any similar accounts), and estate-related assets (boats, furniture, fine art, etc.).

To get the most aid, it is a good idea to move your money from the reportable areas the non-reportable areas before you begin the application process. That said, here are some ways to get more aid:

#1

Money in IRAs and 401(k)s is not considered by FAFSA, so the nest egg is safe! But it may be a good time to increase the nest egg. If you’re thinking ahead, you will begin putting your savings money into your retirement accounts when your kid begins high school, that way, you can fill out the FAFSA with a lower asset base.

This will ensure that you pay less and can take full advantage of money offered though FAFSA. One other benefit of Roth IRAs is that you can use your contributions to pay college bills, tax free.

#2

If you have a large money in your savings account when you begin the FAFSA application process, consider spending some of that money to pay off debts, make extra mortgage payments, or purchase big household items. If you do this, you will reduce your available money for college, thus letting the money from FAFSA pick up more of the tab.

However, keep in mind that FAFSA protects $50,000 worth of assets (depending on your age), so this spending strategy only works well if you’re already a big saver who can spend big. This asset protection allowance has been declining, so it is best to move money if you’re middle- or high-income family.

#3

If you make less than $50,000 per year and your family meets other criteria, you may qualify for more aid based on the simplified needs test. To check your eligibility, you will need 1040A and 1040EZ tax forms from the IRS.

Other indicators that you qualify for more FAFSA aid include other means-tested benefits from the federal government, such as WIC, SNAP, TANF, SSI, or a free/reduced lunch program.

#4

If you have a trustworthy friend or family member who loves your kid and cares about their education and wants to help you out, consider giving them a $14,000 gift (double that if you’re giving the gift to a couple), which is the maximum gift allowance set by the federal government. They're free to use this gift as they see fit.

Whatever you do, stick only to legal financial voodoo to play the game to your advantage - do not lie about your income or your assets on the FAFSA or you risk facing a fraud charge punishable by up to $20,000 dollars, forfeiture of any financial awards, and potential time in prison.

The Department of Education, individual colleges, and the IRS are very, very good at finding fraudulent submissions, so you would do well to stick to trying to improve your financial claims by the legal means listed above rather than to misrepresent your financial picture. When filling out the FAFSA, let your conscience be your guide.

What Can Get Me More FAFSA Money?

There are a few simple tricks and overlooks involved with filling out the FAFSA. Here are some snags that often catch people looking for federal aid.

File Early and Anyway

Take advantage of the new rules regarding filing dates. You can now get a jump on filing beginning in October!

Many states (like Kentucky, Illinois, the Carolinas, Vermont, Washington, and Tennessee) base their financial aid gifts on a first-come, first-served basis, so it's beneficial to get going A-S-A-P on the F-A-F-S-A. As well, file even if you're not sure if you will get aid. Even households earning nearly $200,000 dollars a year can qualify for some kind of aid - every bit helps.

Last year, students left 2.7 billion on the aid table -who wouldn't want a cut of that cash? Lastly, if your family's financial situation shifts while a student is in school, it can be more complicated to get aid later. And don't be afraid to ask for help!

Appealing Isn't Whining

If you don't get the aid you want or need, there's still an opportunity to get more money: an appeal. If your financial status has changed recently, you may qualify. Any kind of change for your financial outlook over the next year can be grounds for appealing - hospitalization, unexpected expenses, major life shifts, etc. You may want to try and appeal to a college financial aid department, too.

If you decide to appeal, be sure that you remember to be polite and humble - leave any feeling of entitlement at the door. And use that supplementary letter to explain any extenuating circumstances. Communication is the name of the game.

Common Mistakes

Lots of folks make some basic mistakes filling out the app. Watch out for these easy mistakes:

- If your parents are divorced or separated, be sure the right one is filling out the document. The parent who has lived with the child for the majority of the year should fill out the form.

- This person is your custodial parent and may or may not necessarily be the legal guardian.

- Be sure to put zeros on the application to negate categories that do not apply to you; do not leave fields of the online or paper app blank.

- The answer "do no know" will be treated as a "no" by the readers of the apps, so if you don't know what something means, be sure to give it a quick Google search. This especially concerns questions related to your parents, like if one is a "dislocated worker." Don't be ashamed of or afraid to disclose your parent's occupational status or level of education.

- Some schools will require other applications besides the FAFSA, like the CSS or even institution-specific documents for financial aid. Be sure to know exactly what your school is looking for and submit the forms on-time to get the maximum amount of aid.

- Entering lots of tax data from scratch is time consuming. Make your life easy and use the IRS Data Retrieval Tool.

Now that you've got that all done, get on to filling out the FAFSA here. It's time to take your first steps toward becoming a college student. Click that link and get started!

Online College Resources

Helping you prepare and gain the most out of your educational experience.